Base is Coinbase’s Layer 2 blockchain built on the Optimism stack, designed to bring the next billion users on-chain. Because it’s backed by one of the largest crypto exchanges and tightly integrated with the Coinbase ecosystem, the possibility of an official Base airdrop has become one of the most anticipated in the crypto space.

While there’s no confirmed airdrop yet, Base has already hinted at rewarding early adopters, creators, and builders who help grow the network. That means your on-chain activity today could pay off later if Base or related ecosystem projects choose to reward contributors.

👉 New to Base? You can Sign up on Coinbase to bridge easily and earn unique Base ecosystem badges along the way.

🧭 How to Potentially Qualify for the Base Airdrop

1️⃣ Trade on Base

Use Base-native DeFi protocols to show consistent activity. Start with Avantis Finance — a trading platform built on Base.

Swap, provide liquidity, or use any available trading features.

Interacting with multiple dApps can increase your eligibility if Base tracks ecosystem engagement.

2️⃣ Build on Base

If you’re a developer, deploying even a small contract on Base is a strong signal of contribution.

Use tools like Remix or Thirdweb to deploy a smart contract.

Participate in Base hackathons or open-source projects.

Complete any available quests or tasks linked to your name. These often become criteria in ecosystem reward programs.

Owning a .base name and completing the associated quests can serve as proof of engagement — and may be included in future reward criteria.

From there, you can build your profile and check your score. You can also get verified if you have a Coinbase account.

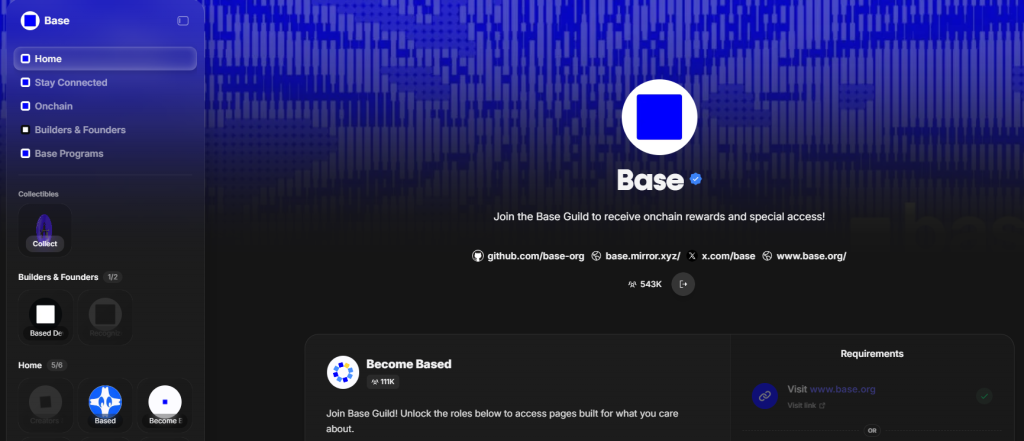

5️⃣ Join the Base Guild

Join the official Base Guild to access community roles and missions.

Connect your wallet and complete tasks (joining Discord, following Base on X, small on-chain actions, etc.).

Earning guild roles shows consistent engagement with the community.

Guild participation has historically been used to identify early supporters in other ecosystems.

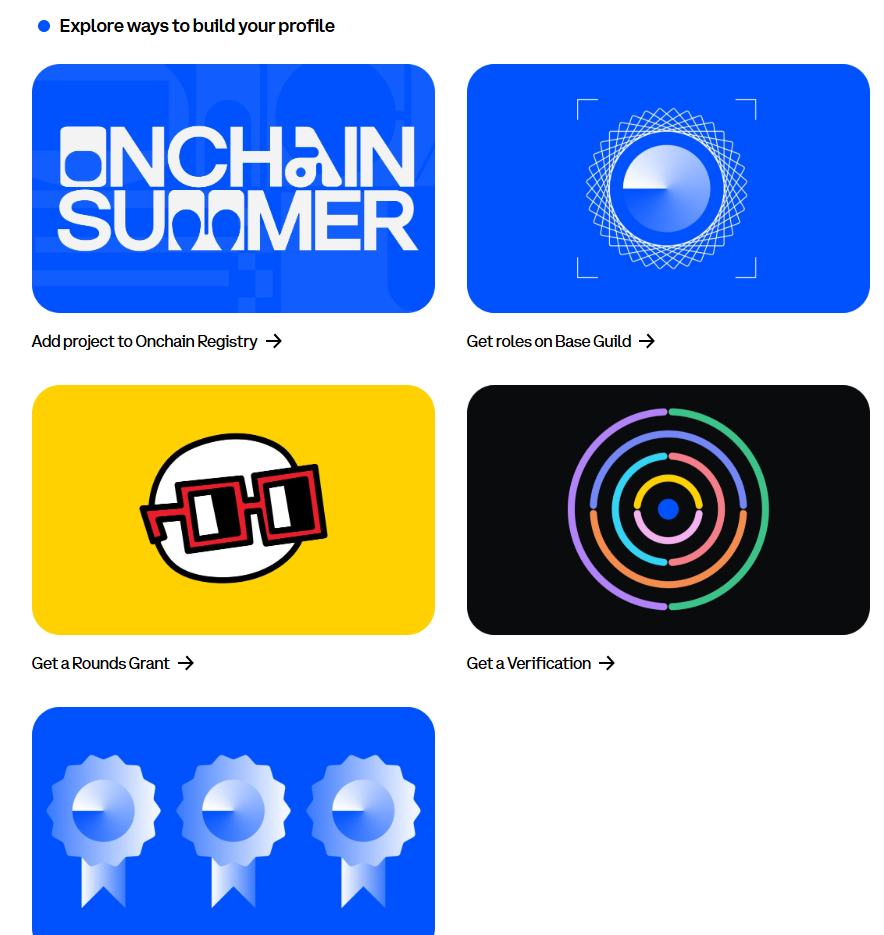

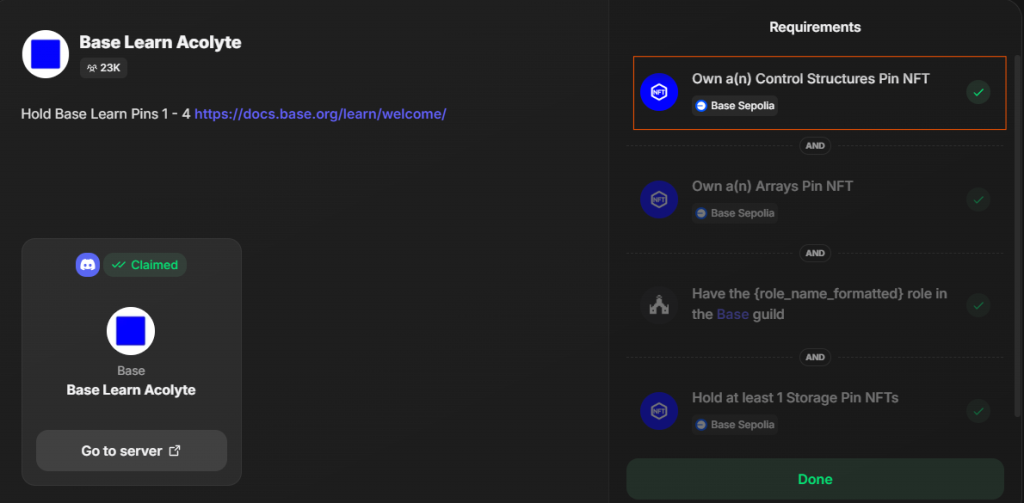

6️⃣ Collect Builder NFTs

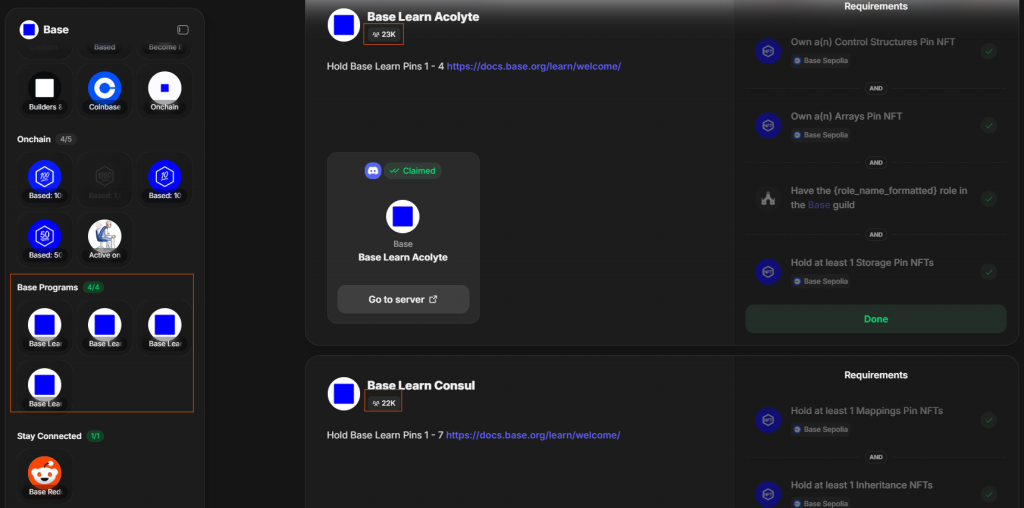

Base has released several Builder NFTs that help identify early contributors. Owning these NFTs could set you apart from other users. The tasks to claim them are listed under “Base Programs”, and far fewer people have completed these compared with other onboarding tasks — so they may be especially valuable to pursue. Below is a step-by-step tutorial on how to claim them.

🧱 How to Claim Your Base Builder NFTs (Testnet Tutorial)

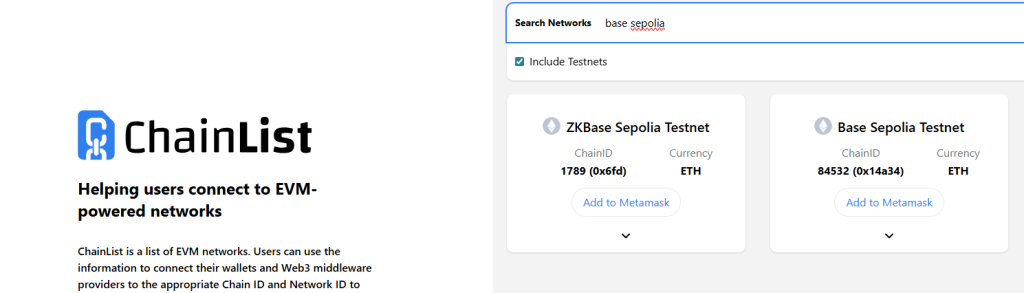

🔹 1. Set Up the Base Sepolia Network

Add the Base Sepolia network to your favorite supported wallet. You can easily add it to metamask through Chainlist.org.

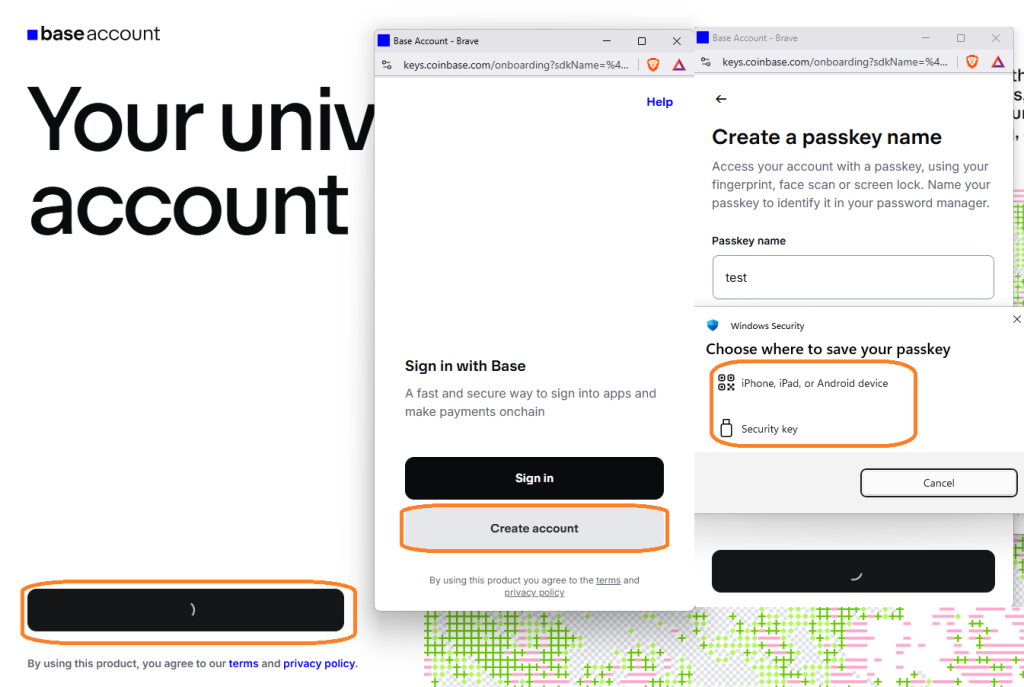

If you prefer, you can also create a Base universal wallet — here’s how:

5. Link both your main wallet and your Base universal account wallet to Guild for seamless progress tracking.

🔹 2. Get ETH on the Testnet

You’ll need a small amount of testnet ETH to deploy your contract. Visit the Base Faucetpage — it offers multiple ways to claim ETH.

If you’re using the Base universal account, your gas fees are often sponsored by Coinbase.

If you have a Coinbase account, you can log in and use their developer faucet.

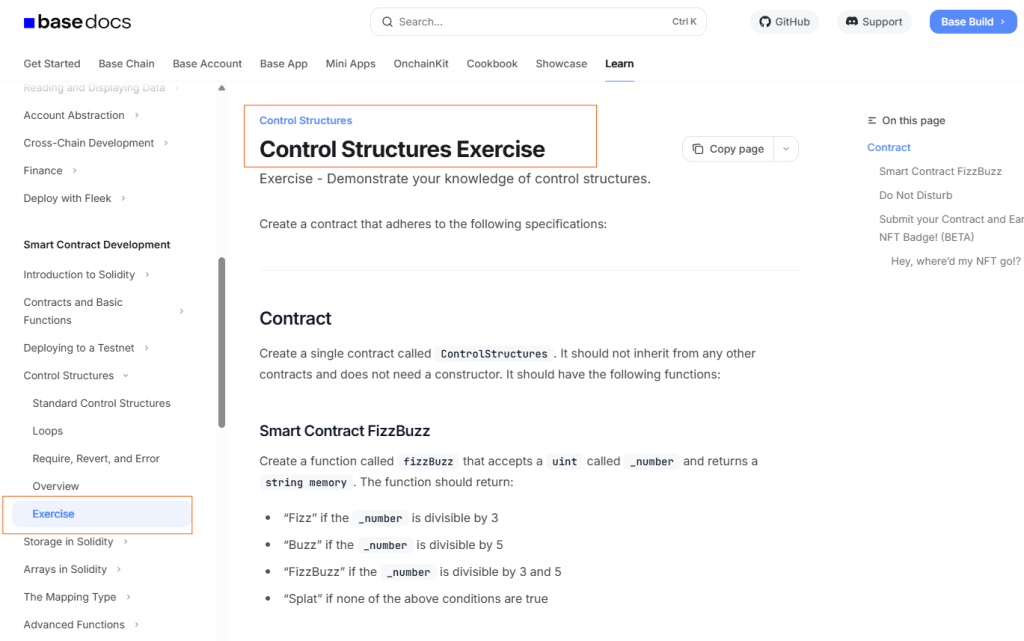

🔹 3. Locate the Builder Exercises

Head to the Base Learn portal. Each Builder task corresponds to an “Exercise” section within the learning module. Find the exercise that matches the task you’re working on — it’s typically under the Exercise tab of that module as seen below.

🔹 4. Write Your Solidity Code

Now, solve the exercise by writing the Solidity contract. Modern tools like AI can help accelerate your learning curve, but make sure you understand each line. ⚠️ Important: Never deploy test contracts from a wallet that holds real assets — always use a fresh or test wallet.

We will provide you with the code for the “Control Structures” exercise.

// SPDX-License-Identifier: MIT

pragma solidity ^0.8.0;

contract ControlStructures {

function fizzBuzz(uint _number) public pure returns (string memory) {

if (_number % 3 == 0 && _number % 5 == 0) return "FizzBuzz";

if (_number % 3 == 0) return "Fizz";

if (_number % 5 == 0) return "Buzz";

return "Splat";

}

error AfterHours(uint time);

function doNotDisturb(uint _time) public pure returns (string memory) {

assert(_time < 2400);

if (_time > 2200 || _time < 800) {

revert AfterHours(_time);

}

if (_time >= 1200 && _time <= 1259) {

revert("At lunch!");

}

if (_time >= 800 && _time <= 1199) return "Morning!";

if (_time >= 1300 && _time <= 1799) return "Afternoon!";

if (_time >= 1800 && _time <= 2200) return "Evening!";

return "";

}

}

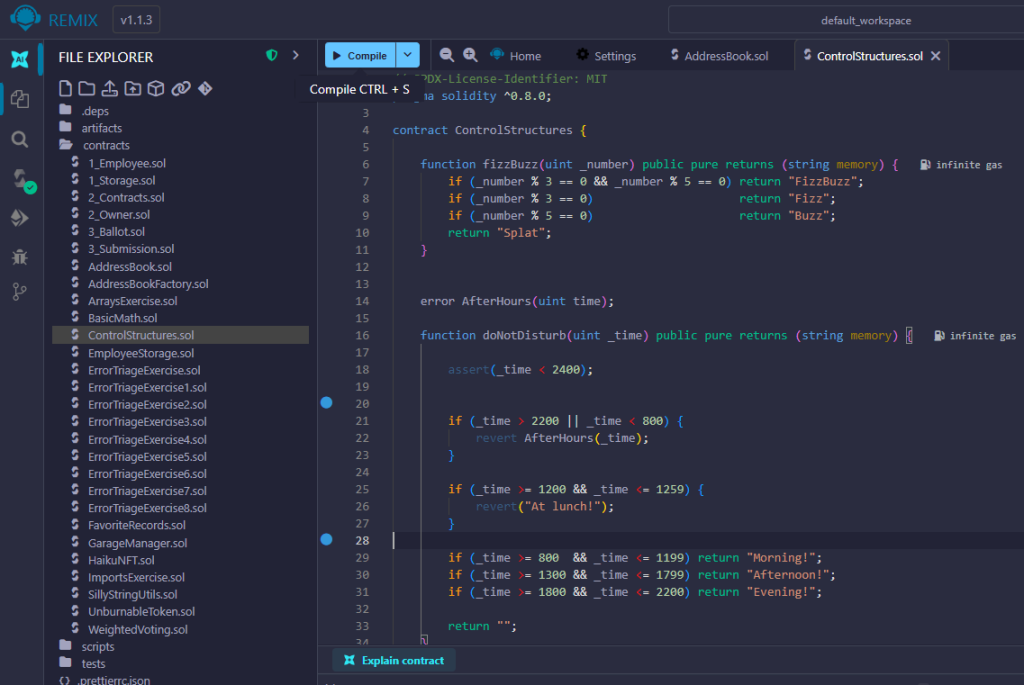

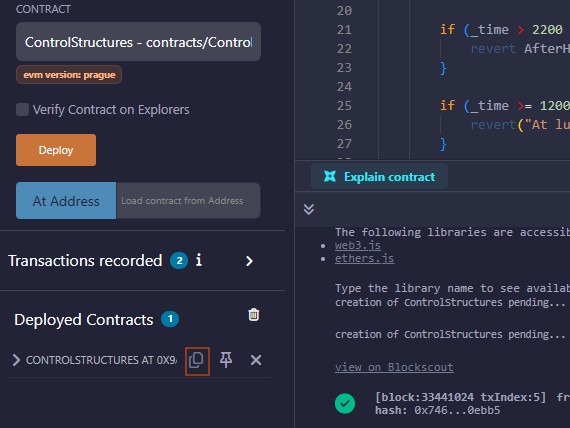

🔹 5. Compile Your Code in Remix

Go to Remix IDE. Under the contracts folder, create a new file — for example, ControlStructures.sol. Paste your Solidity code, and make sure it compiles without errors.

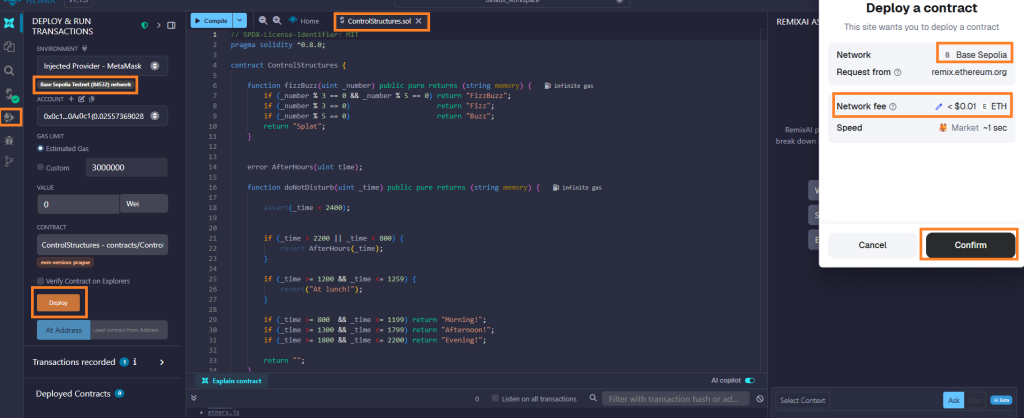

🔹 6. Deploy to Base Sepolia

Open Remix’s Deploy & Run tab. Connect your MetaMask or Base universal wallet to Remix. Select the Base Sepolia network, and deploy your contract. 👉 You can find more deployment guidance on Remix’s Base documentation page.

🔹 7. Find Your Contract Address

Once deployment is complete, scroll down to the Deployed Contracts section. Copy your contract address — you can then view it directly on BaseScan Sepolia.

🔹 8. Verify and Publish (Optional)

Optionally, you can verify and publish your contract on BaseScan. Not all exercises require verification, but doing so helps confirm your work publicly on-chain.

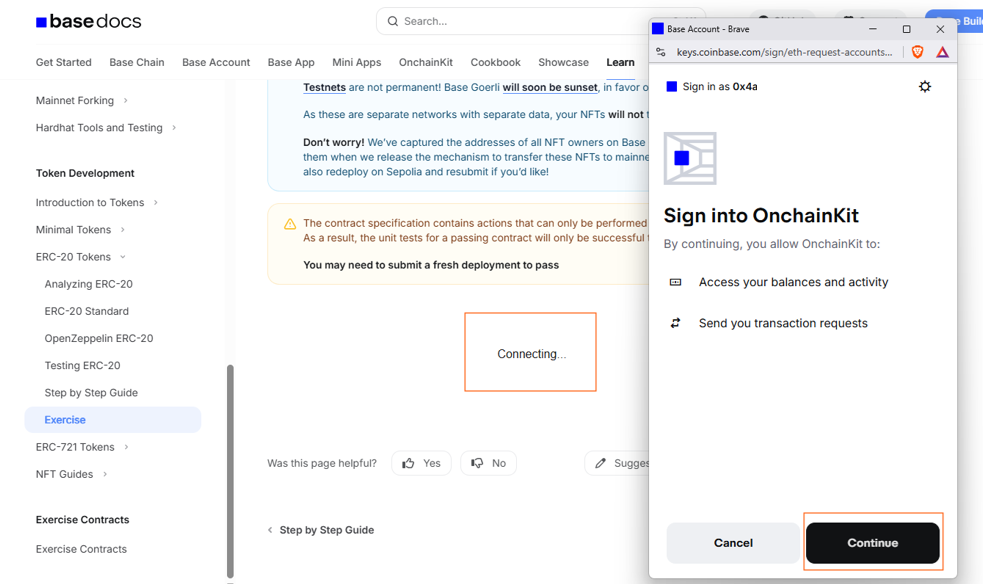

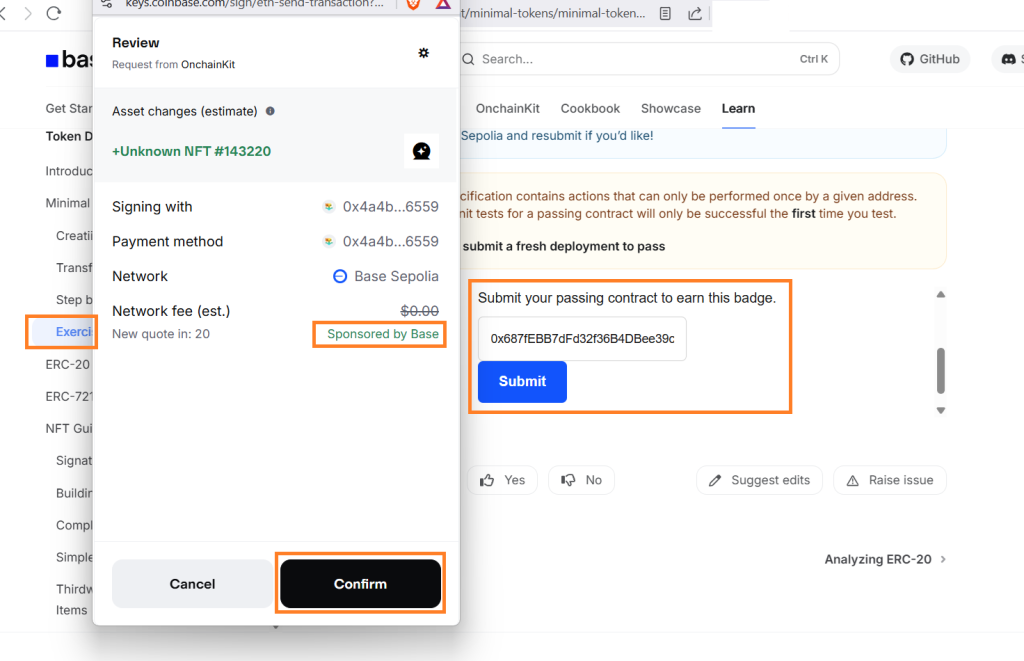

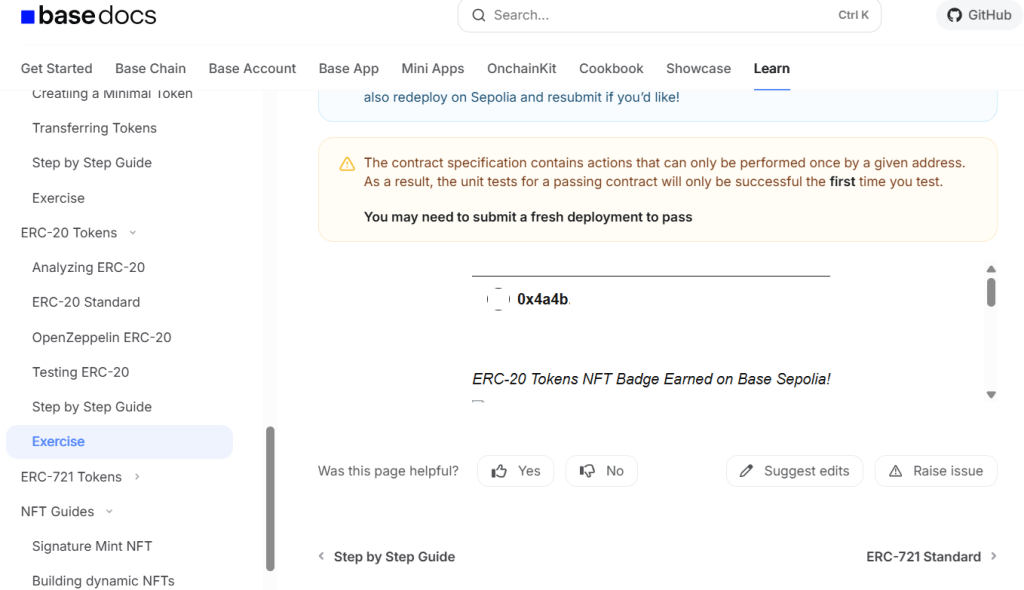

🔹 9. Submit and Claim Your Builder NFT

Go back to the corresponding Exercise page on Base Learn. Scroll to the bottom, connect your Base wallet, and submit your contract address. Once validated, your Builder NFT will be automatically minted to your wallet.

🔹 10. Keep Building and Level Up

Repeat the same process for all exercises to collect more Builder NFTs. When you complete a full set, claim your Builder role on Base Guild. Each completed mission strengthens your on-chain presence — and could make a difference if Base ever rewards early contributors.

🧩 Final Thoughts

There’s no guaranteed Base airdrop — but early users, builders, and creators are always the most likely to be rewarded in any growing blockchain ecosystem.

By trading, building, creating, and joining Base’s community today, you’ll position yourself for any future rewards from Base or its ecosystem partners.

In the wild, 24/7 arena of cryptocurrency trading — where markets never sleep and emotions often lead to costly mistakes — a new player is quietly reshaping how people invest.

Enter avo.so, a Solana-based platform that blends artificial intelligence with decentralized finance (DeFi) to create a marketplace for autonomous trading agents.

No more staring at charts or second-guessing trades — Avo lets you deploy smart AI “agents” that trade on your behalf, mimicking top performers or executing custom strategies.

As of September 2025, with $AVO’s token surging 155% in the past week, the project is riding the wave of AI-meets-DeFi hype. But is it the future of passive investing — or just another flash in the pan? Let’s dive in.

What Is Avo.so? A Quick Origin Story

Launched on Solana — the speed demon of blockchains — Avo emerged as a response to crypto’s core pain point: complexity. Founded by a team of lifelong builders (CEO @0xpaperhead reportedly started coding at age 9), the platform positions itself as “intelligent systems for user-driven crypto investing.”

Think of it as Robinhood meets ChatGPT, but fully on-chain.

Its fair launch in early 2025 was a masterstroke — no massive team allocations, zero VC dumps, just community-first distribution

This ethos led to rapid adoption, Bitget partnerships, and endorsements from creators like @pasternak. Today, Avo’s Discord is buzzing with traders sharing PnL screenshots, while its Telegram mini-app makes onboarding as easy as sliding into a chat.

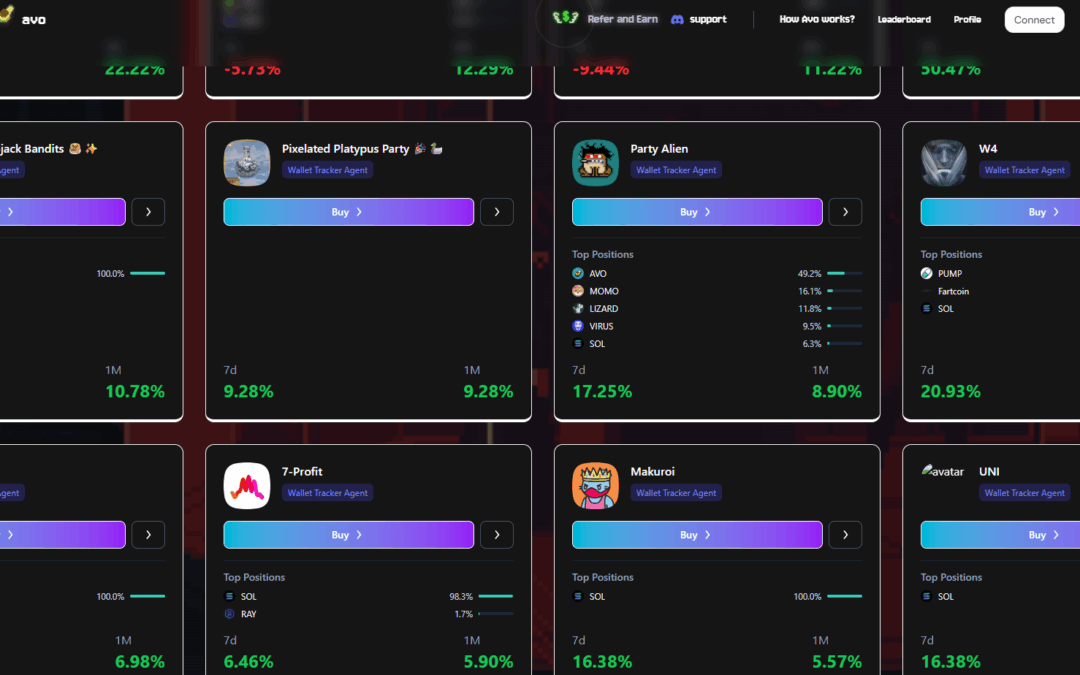

At its heart, Avo isn’t another “bot farm” — it’s a marketplace for AI trading agents, customizable digital sidekicks that handle everything from sniping meme coins to managing diversified portfolios.

With $AVO’s market cap around $15M and 24-hour trading volume exceeding $2M, the blend of AI + Solana = serious momentum.

How Avo.so Actually Works

1️⃣ Connect

Link your Solana wallet (Phantom, Sollet, Backpack) to Avo’s dashboard or Telegram mini-app.

2️⃣ Discover Agents

Browse the marketplace to find wallets, indexes, or AI-driven agents built by top researchers and traders. Filters help you match your risk appetite — from “Degen” to “Guarded.”

3️⃣ Launch

Click “Use Agent.” Avo instantly deploys your chosen agent, which then trades in real time on your behalf.

4️⃣ Manage & Withdraw

Monitor your portfolio, adjust allocations, or withdraw anytime — no lock-ups, full user control.

Protections: Avo integrates liquidity filters to avoid rug pulls and low-liquidity tokens, letting users choose between:

🔥 Degen (minimal protection)

⚖️ Moderate (balanced)

🛡️ Guarded (maximum safety)

Feature

How It Works

User Benefit

Agent Marketplace

Browse/deploy AI agents in-app

Democratizes pro trading for retail users

Copy Trading

Mirror top-performing wallets

Passive income without manual effort

Custom Logic

No-code rule builder + oracle data

Tailor your risk and strategy easily

$AVO Token Utility

Fees, staking, agent rewards

Aligns incentives for long-term holders

Scalability

Solana-optimized infrastructure

Low fees + sub-second execution

Want to List Your Own Agent?

It’s not just for users — developers, traders, and researchers can list their own agents on the marketplace. To do so, creators currently submit a form to the team for vetting and onboarding. This hybrid approach ensures quality control and risk management, preventing spam or malicious bots from flooding the market.

As Avo’s ecosystem matures, expect this to evolve into a fully on-chain listing system — complete with reputation scores, performance stats, and tokenized revenue sharing.

The $AVO Token: Fueling the Avocado Engine

$AVO isn’t just another meme coin. With a 1B total supply and fair launch, it’s deflationary by design — trading fees are burned while high-performing agents receive token rewards.

Current price: ~$0.024, up 73% in 24h

Perks: discounted fees, staking benefits, and airdrop priority

Holders: rapidly growing, with whale accumulation trends visible on-chain

$AVO powers the ecosystem: deploy agents, customize their logic, earn from followers, or stake for governance.

Competitors: Avo vs. the Trading Bot Pack

Platform

Focus

Strengths

Weaknesses

Why Avo Wins

Banana Gun

Telegram sniper bots

Lightning-fast memecoin snipes

High fees, no AI logic

Avo’s AI agents can manage portfolios, not just pumps

Trojan

Copy trading

Simple UX

Limited customization

Avo offers marketplace + oracles for precision

eToro / ZuluTrade

Centralized copy trading

Fiat access, big user base

Custodial, opaque

Avo is DeFi-native and transparent

3Commas / Pionex

Algo grids & signals

Advanced tooling

Expensive subs, clunky UI

Avo is mobile-first, free, and community-driven

Unlike most “bots,” Avo’s agents evolve — they learn, adapt, and can be shared or monetized. It’s less about chasing pumps, more about building sustainable, automated portfolios.

Why Avo Could Be the Next Big Thing

The AI x DeFi narrative is exploding — and Avo sits right at the intersection. Just as Fetch.ai and SingularityNET built billion-dollar agent networks, Avo is doing the same for crypto trading.

Tokenomics Upside: At $0.024, $AVO’s FDV is just ~$24M — tiny compared to AI peers.

Macro Tailwinds: Solana’s TVL racing past $10B and rising retail appetite for automation.

Community Fire: Viral X presence, performance screenshots, and grassroots marketing.

🔴 Risks:

Solana congestion, agent logic bugs, and AI misfires could all impact outcomes. But with non-custodial design and no VC overhang, the downside feels limited.

As usual, there’s always smart contract risks.

🥑 Final Thoughts

Avo isn’t just another AI buzzword play — it’s a genuine attempt to democratize algorithmic trading for the masses.

With V2 coming (custom wallets, enhanced oracles, more agent autonomy), $AVO could be one of Solana’s breakout projects of 2025.

DYOR, NFA — but if you’re tired of manual trading, maybe it’s time to deploy an agent and let the avocados do the work.

Sources: Grok, ChatGPT, CoinGecko, Leap Wallet, Reddit/SolanaSniperBots, X posts from @avodotso & community.

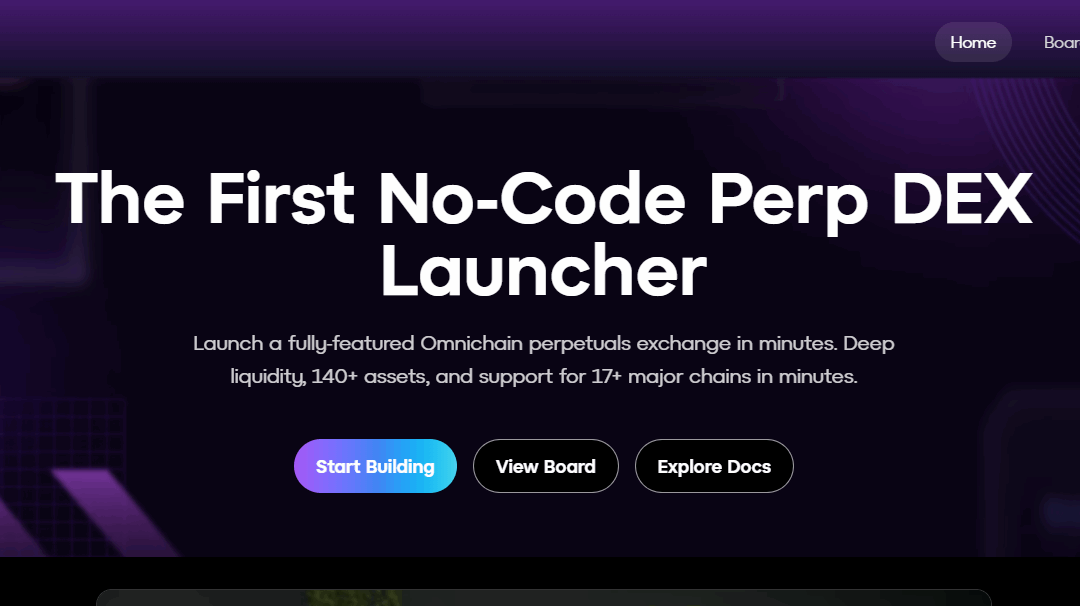

Orderly ONE is a no-code platform that lets DAOs, creators, funds, and communities launch branded perpetual DEXs in minutes. It pairs Orderly Network’s institutional-grade, omnichain liquidity layer (shared CLOB) with an AI-driven customization flow so builders can keep fee revenue and control UX without writing code.

Quick comparison: Orderly ONE vs Aster vs Hyperliquid (HIP‑3)

Orderly ONE — No‑code, white‑label perp DEX launcher built on Orderly’s omnichain, shared central limit order book (CLOB). Boots‑rapped liquidity from professional market makers; free to launch, $1,000 broker code to enable fee capture (discounted in native $ORDER). Low‑latency, self‑custody UX.

Aster — User‑facing perp DEX product offering deep pooled liquidity and advanced trade tools (hidden orders, cross‑chain UX). Primarily an end‑user DEX rather than an infra product for white‑label builders.

Hyperliquid (HIP‑3) — Protocol feature to let builders permissionlessly deploy their own perp DEXs on HyperCore. Deployers must stake a large HYPE bond and will run isolated, deployer‑managed markets with validator slashing protections.

What differentiates Orderly ONE (liquidity infrastructure)

Shared orderbooks (CLOB) aggregate liquidity from institutional market makers, professional traders, and retail — reducing slippage for large trades.

Omnichain routing & aggregator (supports many EVM & non‑EVM chains) to let a single builder offer markets across multiple chains.

CeFi‑grade execution (sub‑200ms latency claims) while keeping on‑chain settlement and self‑custody.

AI customization removes dev friction: brandable UI, fee config, and instant deployment.

Benefits of Orderly ONE vs Hyperliquid HIP‑3 and Aster

Vs Hyperliquid HIP‑3

Lower friction to launch: no huge native token stake or onchain auctions to participate in — Orderly’s monetization is $1k broker code (or token discount) vs Hyperliquid’s 500k HYPE staking requirement.

Shared liquidity: Orderly pools liquidity across builders (reduces fragmentation) rather than creating fully isolated orderbooks per deployer.

Bootstrapped market makers & operations: Orderly supplies routing and liquidity primitives; HIP‑3 leaves much of market ops and risk settings to the deployer (and validators can slash).

Vs Aster

White‑label focus: Orderly is infrastructure-first — it enables other brands to run DEXs under their own name and capture fee revenue.

Monetization for communities: Orderly advertises the ability for communities to keep 100% of trading fees and fully configure fee tiers.

Plug‑and‑play for builders: Aster is a product DEX you can list on; Orderly is the tool to create many DEXs quickly.

Pricing & revenue split

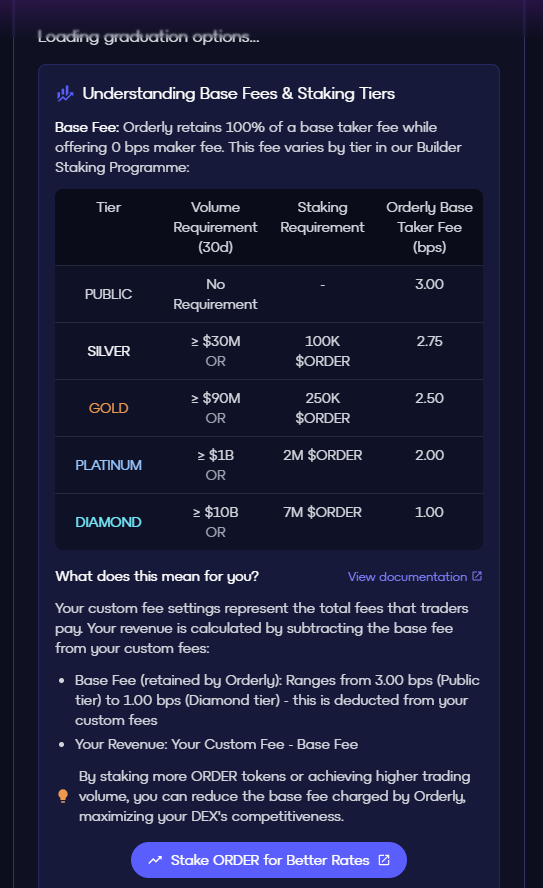

Orderly ONE: Launching a DEX is free; to receive a broker code (needed to earn fee revenue) you pay $1,000 or use $ORDER for a 25% discount. Builders can set their own fee schedule and capture the revenue (Orderly markets the “capture 100% of trading fees” value prop). In addition, staking $ORDER unlocks further trading fee reductions for end users and may increase the share of rebates builders receive. This creates an incentive loop where communities benefit both from lower user costs and higher builder revenue retention.

Hyperliquid HIP‑3: Deployers must maintain a 500,000 HYPE stake; the deployer may set a fee share of up to 50% (fee share is configurable in the protocol docs). There are also Dutch auction mechanics for additional asset listings.

Aster: Public docs emphasize deep pooled liquidity and product features; revenue split/partner payout details are product‑specific (not a white‑label revenue model like Orderly ONE).

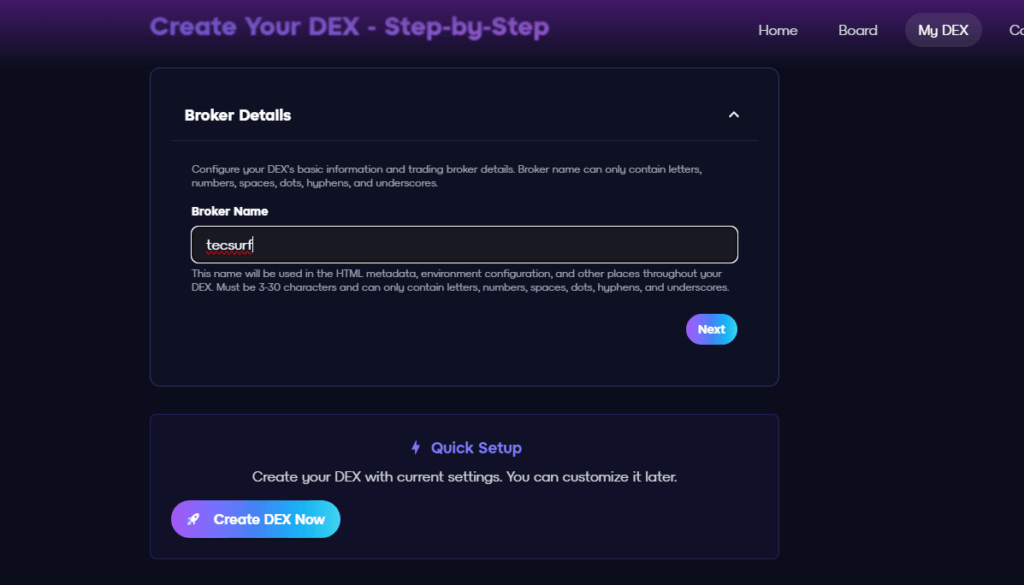

Launch a Perp DEX in Minutes with Orderly ONE

Here are the basic steps:

Visit orderly dex builder page and Sign up with your wallet:

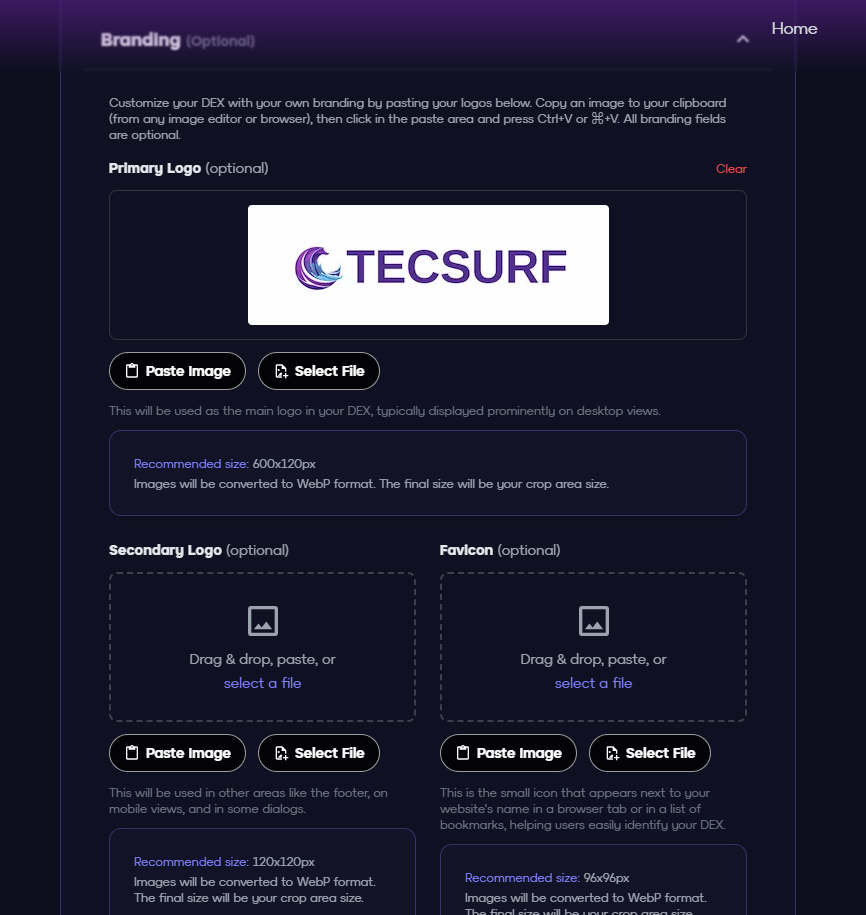

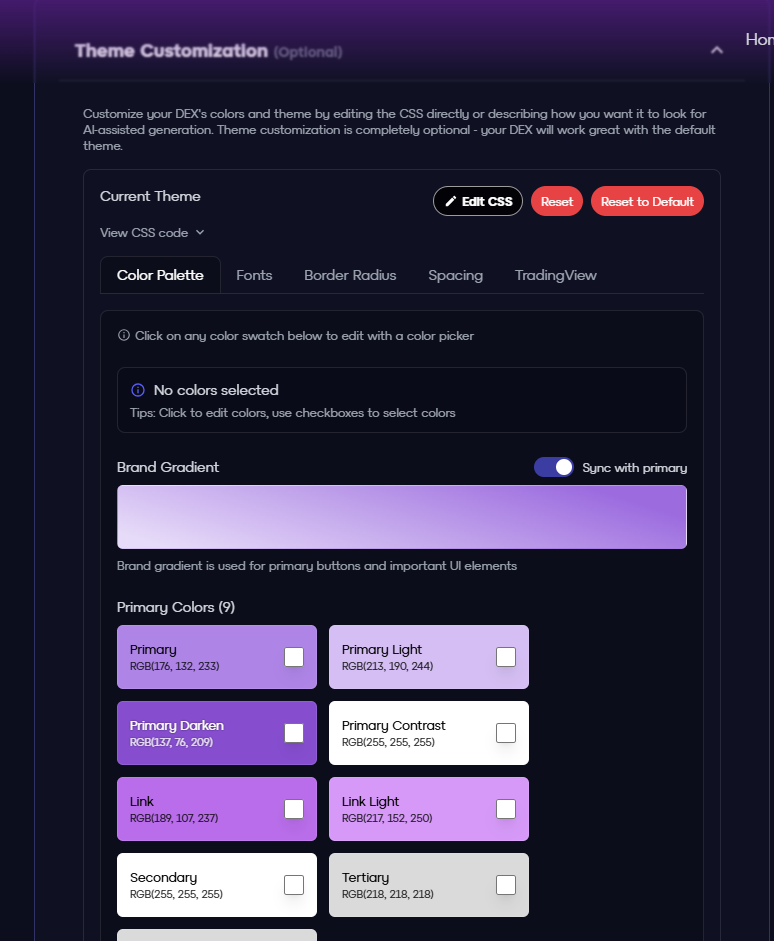

Choose your dex name and choose your theme colors, you can even use AI to describe your theme and it will be generated:

You can then configure your socials, walletconnect, privy and SEO.

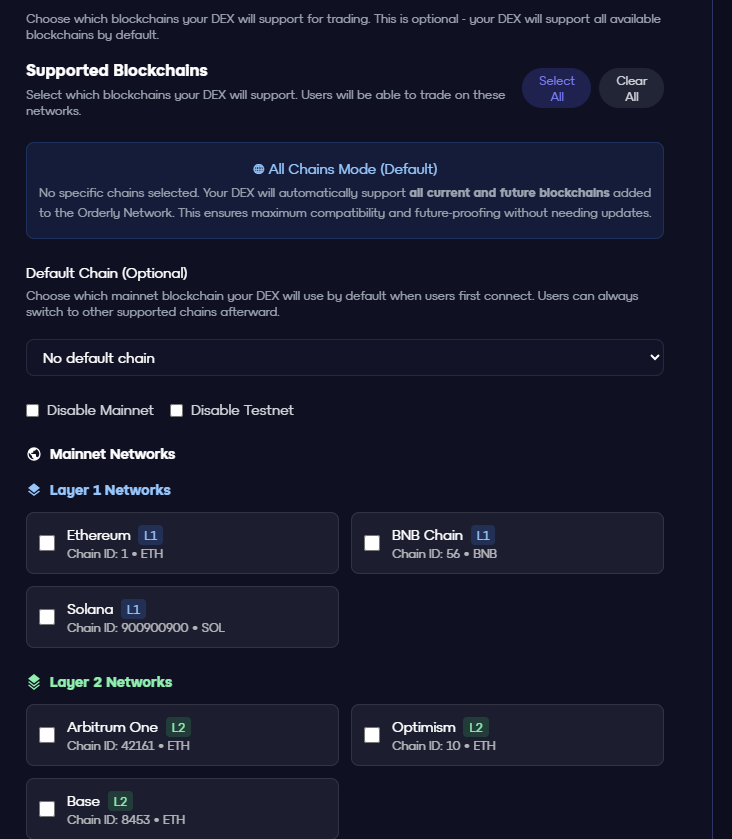

Then you can choose which blockchains you want to include in your perp and navigation menu. You can then proceed to create your perp.

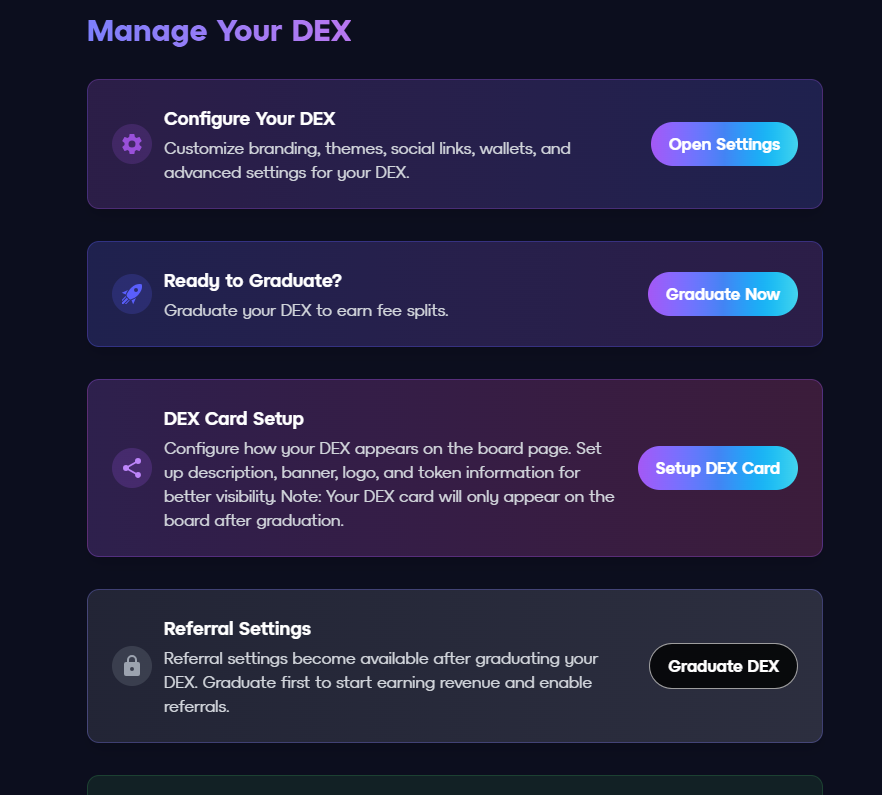

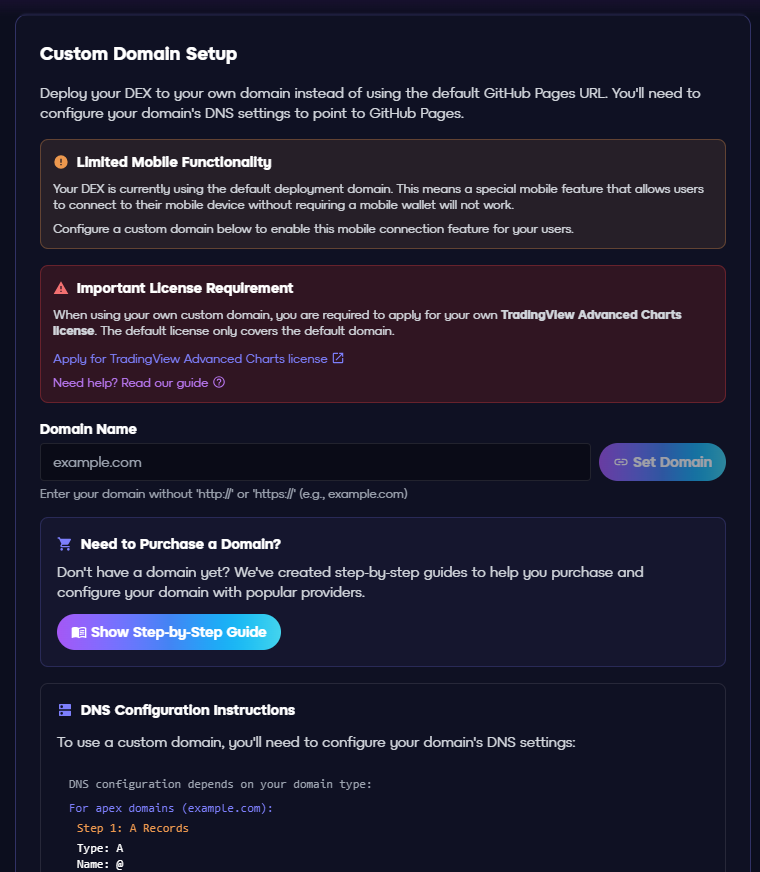

To start earning revenue, you need to graduate your dex and pay the fees. You can also use your custom domain name:

The steps are easy to follow and you can change any configuration later on. You can find more documentation here.

In our recent article on Bittensor’s TAO vs. centralized AI powerhouses, we explored a stark contrast: trillion-dollar data centers controlled by a handful of corporations versus an open, tokenized marketplace of distributed intelligence. But there may be a third contender quietly emerging — not in crypto, but in the garages, driveways, and streets of Tesla’s global fleet.

With millions of vehicles equipped with powerful GPUs for Full Self-Driving (FSD), Tesla possesses one of the largest untapped compute networks on the planet. If activated, this network could blur the line between centralized and decentralized AI, creating a new hybrid model of intelligence infrastructure.

Today’s Reality: Closed and Centralized

Right now, Tesla’s car GPUs are dedicated to autonomy. They process vision and navigation tasks for FSD, ensuring cars can see, plan, and drive. Owners don’t earn revenue from this compute; Tesla captures the value through:

FSD subscriptions ($99–$199 per month)

Vehicle sales boosted by AI features

The soon-to-launch Tesla robotaxi network, where Tesla takes a platform cut

In other words: the hardware belongs to the car, but the economic upside belongs to Tesla.

Musk’s Teasers: Distributed Compute at Scale

Elon Musk has hinted at a future where Tesla’s fleet could function as a distributed inference network. In principle, millions of idle cars — parked overnight or during work hours — could run AI tasks in parallel.

This would instantly make Tesla one of the largest distributed compute providers in history, rivaling even hyperscale data centers in raw capacity.

But here’s the twist: unlike Bittensor’s permissionless open market, Tesla would remain the coordinator. Tasks, payments, and network control would flow through Tesla’s centralized system.

The Middle Ground: Centralized Coordination, Distributed Hardware

If Tesla pursued this model, it would occupy a fascinating middle ground:

Not fully centralized – Compute would be physically distributed across millions of vehicles, making it more resilient than single-point mega data centers.

Not fully decentralized – Tesla would still dictate participation rules, workloads, and payouts. Owners wouldn’t directly join an open marketplace like Bittensor; they’d plug into Tesla’s walled garden.

This hybrid approach could:

Allow owners to share in the upside, earning credits or payouts for lending idle compute.

Expand Tesla’s revenue beyond mobility, turning cars into AI miners on wheels.

Position Tesla as both a transport company and an AI infrastructure giant.

Robotaxi + Compute: Stacking Revenue Streams

The real intrigue comes when you combine robotaxi revenue with distributed compute revenue.

A Tesla could earn money while driving passengers (robotaxi).

When idle, it could earn money running AI tasks.

For car owners, this would transform a depreciating asset into a self-funding, income-generating machine.

Challenges Ahead

Of course, this vision faces hurdles:

Energy costs – Would owners pay for the electricity used by AI tasks?

Hardware partitioning – Safety-critical driving compute must stay isolated from external workloads.

Profit sharing – Tesla has little incentive to give away margins unless it boosts adoption.

Regulation – Governments may view distributed AI compute as a new class of infrastructure needing oversight.

Tesla vs. Bittensor: A Different Future

Where Bittensor democratizes AI through open tokenized incentives, Tesla would likely keep control centralized — but spread the hardware layer globally.

Bittensor = open marketplace: Anyone can contribute, anyone can earn.

Tesla = closed network: Millions can participate, but only under Tesla’s rules.

Both models break away from the fragile skyscrapers of centralized AI superclusters. But their philosophies differ: Bittensor empowers contributors as stakeholders; Tesla would empower them as platform participants.

Centralized AI vs. Tesla Fleet Compute vs. Bittensor

Feature

Centralized AI (OpenAI, Google)

Tesla Fleet Compute (Potential)

Bittensor (TAO)

Control

Fully centralized, corporate-owned

Centralized by Tesla, distributed hardware

Decentralized, community-governed

Scale

Massive, but limited to data centers

Millions of vehicles worldwide

Growing global subnet network

Resilience

Vulnerable to single-point failures

More resilient via physical distribution

Highly resilient, peer-to-peer

Incentives

Profits flow to corporations

Owners may share revenue (compute + robotaxi)

Open participation, token rewards

Access

Proprietary APIs, restricted

Tesla-controlled platform

Permissionless, anyone can join

Philosophy

Closed & profit-driven

Hybrid: centralized rules, distributed assets

Open & meritocratic

Example Revenue

Cloud services, API subscriptions

FSD subs, robotaxi fares, possible compute payouts

TAO emissions, AI marketplace fees

The Horizon: A New Compute Economy?

If Tesla flips the switch, it could create a new middle path in the AI landscape — a centralized company orchestrating a physically decentralized fleet.

It wouldn’t rival Bittensor in openness, but it could rival Big Tech in scale. And for Tesla owners, it could mean their vehicles don’t just drive them — they also work for them, mining intelligence itself.

Artificial intelligence has become the infrastructure of modern civilization. From medical diagnostics to financial forecasting to autonomous vehicles, AI now powers critical systems that rival electricity in importance. But beneath the glossy marketing of Silicon Valley’s AI titans lies an uncomfortable truth: today’s AI is monopolized, centralized, and fragile.

Against this backdrop, a new contender is emerging—not in corporate boardrooms or trillion-dollar data centers, but in the open-source, blockchain-powered ecosystem of Bittensor. At the center of this movement is TAO, the protocol’s native token, which functions not just as currency but as the economic engine of a global, decentralized AI marketplace.

As Bittensor approaches its first token halving in December 2025—cutting emissions from 7,200 to 3,600 TAO per day—the project is drawing comparisons to Bitcoin’s scarcity-driven rise. Yet TAO’s story is more ambitious: it seeks to rewrite the economics of intelligence itself.

Centralized AI Powerhouses: Titans with Fragile Foundations

The Centralized Model Today’s AI landscape is dominated by a handful of companies—OpenAI, Google, Anthropic, and Amazon. Their strategy is clear: build ever-larger supercomputing clusters, lock in data pipelines, and dominate through sheer scale. OpenAI’s Stargate project, a $500 billion bet on 10 GW of U.S. data centers, epitomizes this model.

But centralization carries steep costs and hidden risks:

Economic Barriers – The capital required to compete is astronomical. Training frontier models like GPT-4 costs upward of $100 million, with infrastructure spending in the billions. This effectively locks out smaller startups, concentrating innovation in a few corporate hands.

Data Monopoly – Big Tech controls the largest proprietary datasets—Google’s search archives, Meta’s social graph, Amazon’s consumer data. This creates a closed feedback loop: more data → better models → more dominance. For the rest of the world, access is limited and increasingly expensive.

Censorship & Control Risks – Centralized AI is subject to corporate and political agendas. If OpenAI restricts outputs or Anthropic complies with government directives, the flow of intelligence becomes filtered. This risks creating a censored AI ecosystem, where knowledge is gated by a few powerful actors.

Systemic Fragility – The model resembles the financial sector before 2008: a handful of players, each “too big to fail.” A catastrophic failure—whether technical, economic, or regulatory—could ripple through industries that rely on these centralized AIs. Billions in stranded assets and disrupted services would follow.

The Decentralized Alternative Bittensor flips this script. Instead of pouring capital into singular mega-clusters, it distributes tasks across thousands of nodes worldwide. Intelligence is openly contributed, scored, and rewarded through the Proof of Intelligence mechanism.

Where centralized AI is vulnerable to censorship and collapse, Bittensor is adaptive and antifragile. Idle nodes can pivot to new tasks; contributors worldwide ensure redundancy; incentives drive continual innovation. It’s less a fortress and more a living, distributed city of intelligence.

📊 Centralized AI vs. Bittensor (TAO)

Category

Centralized AI (OpenAI, Google, Anthropic)

Decentralized AI (Bittensor TAO)

Infrastructure

Trillion-dollar data centers, tightly controlled

Distributed global nodes, open access

Cost of Entry

$100M+ to train frontier models, billions for infra

Anyone can contribute compute/models

Data Ownership

Proprietary datasets, hoarded by corporations

Open, merit-based contributions

Resilience

Single points of failure, fragile to outages/regulation

Adaptive, antifragile, redundant nodes

Governance

Corporate boards, shareholder-driven

Token-staked community governance

Censorship Risk

High – subject to political & corporate pressure

Low – distributed contributors worldwide

Innovation

Innovation bottlenecked to few elite labs

Permissionless, global experimentation

Incentives

Profits concentrated in Big Tech

Contributors rewarded directly in TAO

Analogy

Skyscraper: tall but fragile

City: distributed, adaptive, resilient

The Mechanics of TAO: Scarcity Meets Utility

Like Bitcoin, TAO has a fixed supply of 21 million tokens. Its functions extend far beyond speculation:

Fuel for intelligence queries – Subnet tasks are priced in TAO.

Staking & governance – Token holders shape the network’s evolution.

Incentives for contributors – Miners and validators earn TAO for producing valuable intelligence.

Upgrades like the Dynamic TAO (dTAO) model tie emissions directly to subnet performance, rewarding merit over hype. Meanwhile, EVM compatibility unlocks AI-powered DeFi, merging decentralized intelligence with tokenized finance.

Already, real-world applications are live. The Nuance subnet provides social sentiment analysis, while Sturdy experiments with decentralized credit markets. Each new subnet expands TAO’s utility, compounding its value proposition.

The Investment Case: Scarcity, Adoption, and Network Effects

Bittensor’s bullish thesis rests on three pillars:

Scarcity – December’s halving introduces hard supply constraints.

Adoption – Over 50 subnets are already operational, each creating new demand for TAO.

Network Effects – As contributors join, the intelligence marketplace becomes more valuable, drawing in further participants.

Institutional validation is mounting:

Europe’s first TAO ETP launched on the SIX Swiss Exchange.

Firms like Oblong Inc. are already acquiring multimillion-dollar TAO stakes.

Price forecasts reflect this momentum, with analysts projecting $500–$1,100 by year-end 2025 and potential long-term valuations above $7,000 if Bittensor captures even a sliver of the $1 trillion AI market projected for 2030.

Decentralized AI Rivals: How TAO Stacks Up

Bittensor is not alone in the decentralized AI (DeAI) space, but its approach is distinct:

While Render and Akash provide raw compute, Bittensor adds the intelligence layer—a marketplace for actual cognition and learning. Community consensus is clear: the others could function as subnets within Bittensor’s architecture, not competitors to it.

Historical Parallel: From Mainframes to Decentralized Intelligence

Technology has always moved from concentration to distribution:

Mainframes (1960s–70s): Computing power locked in corporate labs.

Personal Computing (1980s–90s): PCs democratized access.

Cloud (2000s–2020s): Centralized services scaled globally, but reintroduced dependency on corporate monopolies.

Decentralized AI (2020s–): Bittensor represents the next shift, distributing intelligence itself.

Just as the internet shattered the control of centralized telecom networks, decentralized AI could dismantle the stranglehold of Big Tech’s AI empires.

Risks: The Roadblocks Ahead

No revolution comes without obstacles.

Validator concentration threatens decentralization if power clusters among a few players.

Speculative hype risks outpacing real utility, especially as crypto volatility looms.

Regulation remains a wildcard; governments wary of ungoverned AI may impose restrictions on DeAI protocols.

Still, iterative upgrades—like dTAO’s merit-based emissions—are steadily addressing these concerns.

The Horizon: TAO as the Currency of Intelligence

Centralized AI may dominate headlines, but its vulnerabilities echo the financial sector’s “too big to fail” problem of 2008. Bittensor offers an alternative—a decentralized bailout for intelligence itself.

If successful, TAO won’t just be a speculative asset. It will function as the currency of thought, underpinning a self-sustaining economy where intelligence is bought, sold, and improved collaboratively.

The real question isn’t whether decentralized AI will rise—it’s who will participate before the fuse is lit by the halving.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behaviour or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.